Bin Chicken Bonds - Who has Blue Owl in their super?

There are a lot of headlines, podcasts, news segments, articles and reports about Private Credit, none of them good.

And of these headlines, the poster bird for the Private Credit’s ruffled feathers appears to be Blue Owl.

Ruffled Feathers

In short, Blue Owl are the ornithological focal point for two reasons somewhat unique to Blue Owl:

The Saaspocalypse: Blue Owl have significant amounts of high-risk loans to software businesses. (The same businesses that some investors believe are under serious threat from AI companies like Anthropic’s Claude and others). Thus, these highly levered businesses with minimal hard assets might find it hard to service or repay their debt, the debt which they owe to Blue Owl…

Ma & Pa: Blue Owl has comparatively high amounts of individual aka retail investors, as opposed to institutional pension funds, who whilst in turn might generate higher fees for managers like Blue Owl, have significantly different liquidity profiles.

And one reason not unique to Blue Owl:

Private credit in general, potential conflict of interests between managers & investors, exposure to private equity, explosive growth potentially coming at the expense of deteriorating credit / loan quality, opaqueness of loans/fees/investments/disclosures/valuations, lack of liquidity and the general fact we are facing potential economic headwinds which could have meaningful impact on inflation and thus interest rates.

It’s worth noting Blue Owl are a well known, well resourced, experienced global investor, over one thousand of staff, are listed on the New York Stock Exchange, manage over two hundred of billion USD of assets, of which USD $145.5b is in credit, and predominantly operate in the USA - which oddly enough arguably features more stringent regulations than Australia in this field.

If you want the best summary of the inherent problems of private credit, consider Unstructured Capital’s immortal summary below (Good Work’s is also excellent):

Gated

The primary problem facing private credit funds, not just Blue Owl, is the funds being “Gated”. Because private credit is again, private, you can’t sell it as readily as a government bond, or a listed share.

Accordingly, if a large amount of investors rush for the exit at once, the fund might not be able to ‘liquidate’ (sell) the assets to fund the withdrawals, and thus, the fund shuts its ‘Gates’.

This is one of (read about fees below) the reasons that individual investors are not as well-suited to this investment.

The investor’s money is there, it’s just stuck there. They have to wait.

This has happened with Blue Owl, Ares, Apollo, Blackrock, Morgan Stanley and others.

Let the Weasley Family’s Owl from Harry Potter illustrate what this looks like when a bunch of investors try to get their money out.

I have zero idea if the funds mentioned below are gated or not - I am not an investor in any of the funds detailed.

Now, there is a serious difference between a massive, multibillion-dollar pension fund having a small amount in a ‘gated’ fund, versus a Mum & Dad Investor (even if they are HNW or UHNW).

Because it’s debt, you’re still likely to get some investment return back, the problem is time - it can take years.

Migrating South

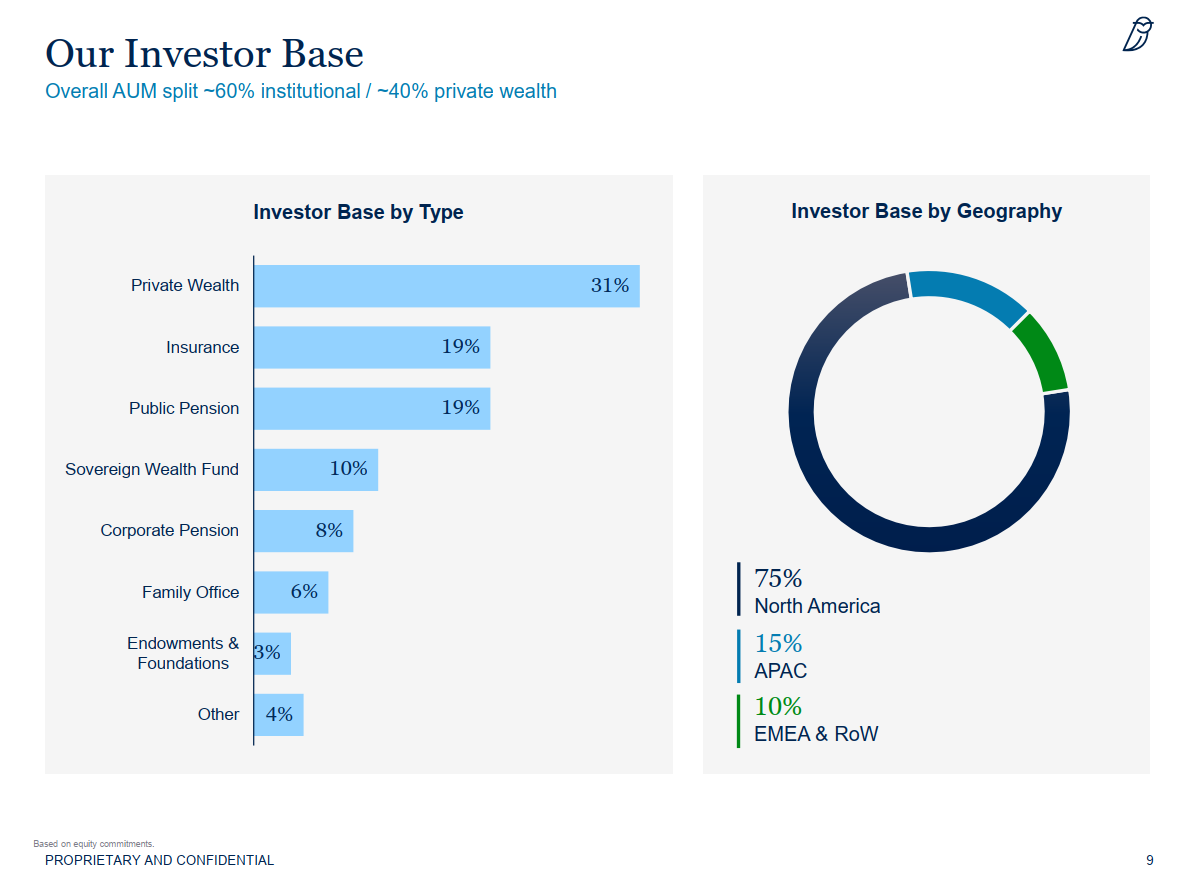

Despite being based in the US of A, Blue Owl, like it’s feathered friends has migrated all over the world.

And of the world, it is the parts inhabited by Wombats that I am most interested in. This would be classified by Blue Owl as APAC, i.e. Asia-Pacific, namely, China, India, Japan, Indonesia, Australia, South Korea - who apparently at last count comrpise 15% of Blue Owl’s investor base.

Which in turn begs the question, Down Under, who has Owl Poo on their portfolio’s windscreen?

NGS Super - Not Gryffindor

On the super front, as far as I can tell that would apparently be NGS Super who across eleven of their options (super & pension), per their 31 December 2025 Portfolio Holding Disclosures have about ~$226,279,315 in total of the in the news & unloved manager.

With decent allocation sizing for an insto investor, ranging from 1.50% for the MySuper options and up to 2.67% for the Diversified Bond Option.

Noting by comparison to the accum Diversified Bond option’s rather rambunctious 15.23% or $5,390,648 allocation to Blackstone Credit Systematic Strategies LLC seems rather mild, dare I even say, chicken (it’s not, it’s just that 15.23% with one manager is ((again, manager, not necessarily single fund or ‘strategy’) is a lot).

Now, fundamentally, NGS’s Portfolio Holdings Disclosures list per manager. This means, they might have 1.50% or 2.67% etc spread across multiple different funds, different strategies. This is not a problem.

Additionally, because NGS are a big investor, they will typically negotiate significantly lower fees, and often a better product than individuals are able to access (less layers).

Given NGS manages $16 billion and is an institutional investor with circa 115,000 members, and is thus well-suited to private credit’s lack of liquidity, this is not reckless nor problematic.

Worth mentioning, the last time I saw an owl in a Non-Government School (NGS FYI) was Ron Weasley’s Howler from the Chamber of Secrets.

Please Note: This is infuriating as I tried to find the scene from Tinker, Tailor, Soldier, Spy where Jim Prideaux kills the Owl in the classroom, but that scene is not on YouTube) - absolutely spewin.

Wing Man

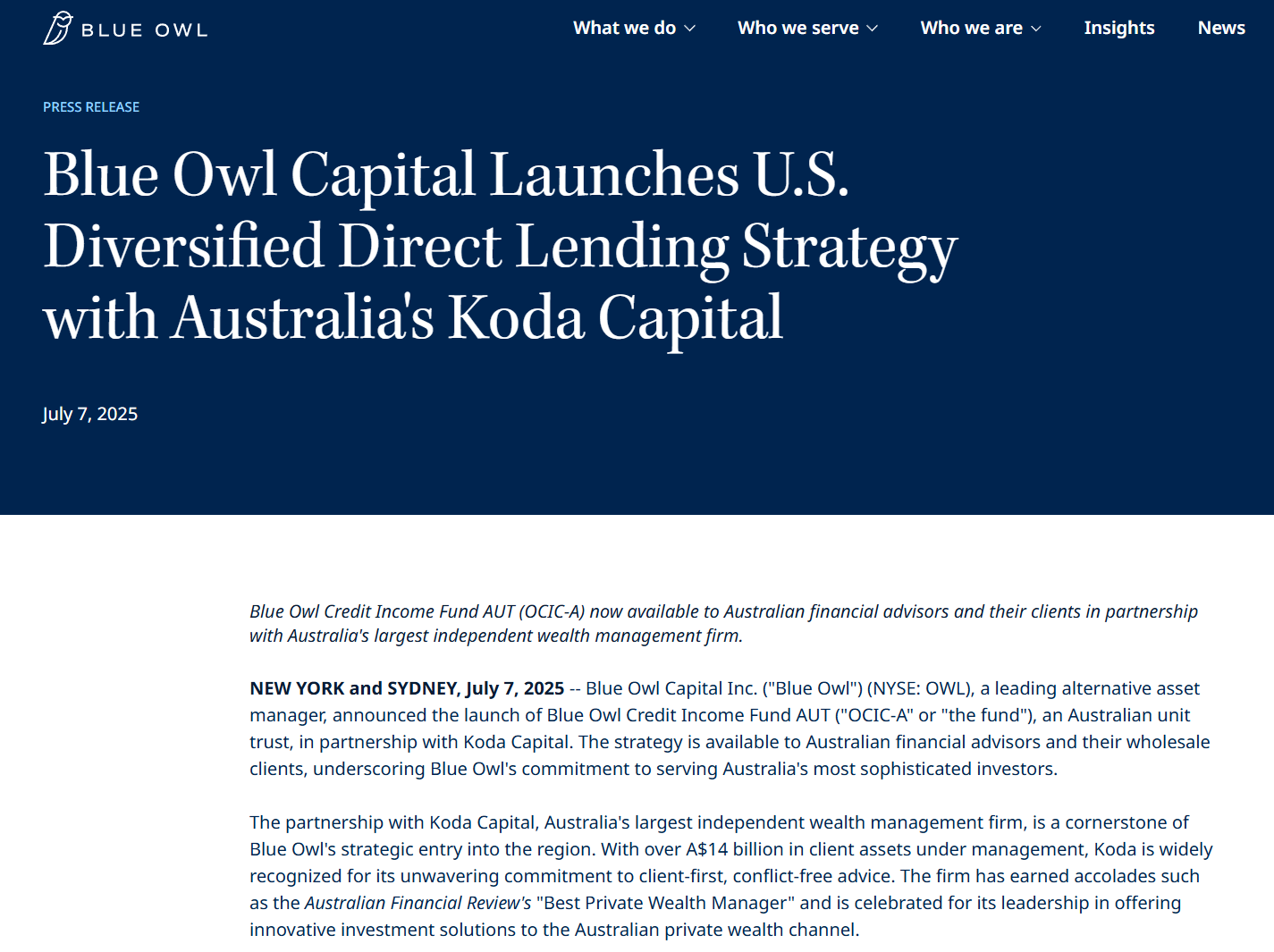

At what I consider the more interesting end, we have Blue Owl’s wingman in Australia, Koda Capital, which, in conjunction with Channel Capital appear to have flown Blue Owl Credit Income Fund AUT down under, which after launching on 30 April 2025, swelled from $52 million at 30 June 2025 to approximately $223,000,000 as at 28th February 2026 (Lonsec). Not bhed.

I can’t get any info on the other Blue Owl offering on Channel Capital’s website, noting it appears to have launched later.

Source: Blue Owl

Peckish for Fees

It would seem that Koda Capital, Channel Capital & Blue Owl have hatched a Fund of Funds.

Generally, I’m not a huge fan of fund of funds.

Mostly because fund of funds tend to take high-risk, highly complicated, extremely expensive, very opaque and mostly illiquid investments, and make them even more complicated, even more expensive, even more opaque and I would argue by virtue of the former, even more illiquid and even more high risk.

I’m not implying Koda Capital receives any benefits in the slightest, and there’s no implication that any fees charged or paid to or Channel Capital as the responsible entity are unusual, high or anything else. This is just generally speaking one of the risks of fund of funds, and it is heightened when considering ‘Alternatives’ like Private credit.

Heads I Win, Tales You Lose

With Funds of Funds - the fees that are paid by individual investors can often become, via layering, quite obscene and we get a prime example of this for Blue Owl’s Credit Income Fund AUT Class A Units (APIR Code CHN8005AU).

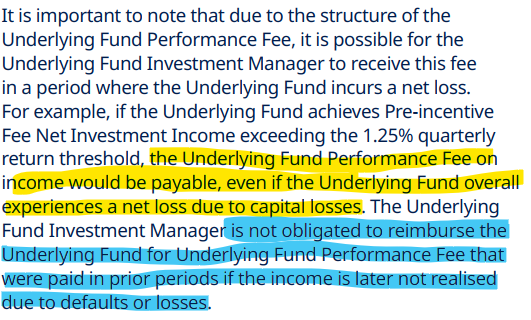

Firstly, Blue Owl’s CHN8005A is the first fund I’ve ever personally seen that pays a performance fee paid Quarterly. (That could be commonplace but I sincerely hope it is not). I only recently saw my first bi-annual performance fee and was revolted.

Personally, I think the very idea of paying a performance fee quarterly is a complete joke. Put simply, Blue Owl’s underlying fund, appears to pay 12.50% of any net income over 1.25% for the quarter. Do you think a lender earning more than 6% annualised interest is incredible? I don’t know the repayment terms. What if big or multiple payments fall in one quarter? How is this fair to investors?

What’s more obscene is paying two different kinds of performance fees.

Blue Owl’s CHN8005AU seems to have the convoluted structure that permits the underlying fund to separate performance fees on income (quarterly) and capital gains (annually) - or at least that’s what’s outlined by the PDS.

The underlying fund charges different performance fees, separately for both income and capital growth.

This means the fund can lose money in a year, and still pay a performance fee. That doesn’t sound like performance entitled to EXTRA fees (Blue Owl and get management fees and other costs regardless of performance).

This is the issue with so many layers, things become murky.

Playing devil’s advocate, someone might argue - ‘the fund is an income-focused product, thus, having separate fees is appropriate’ - I can see the logic, but if it’s an income-focused product, don’t charge on capital gains at all, and regardless, don’t charge quarterly.

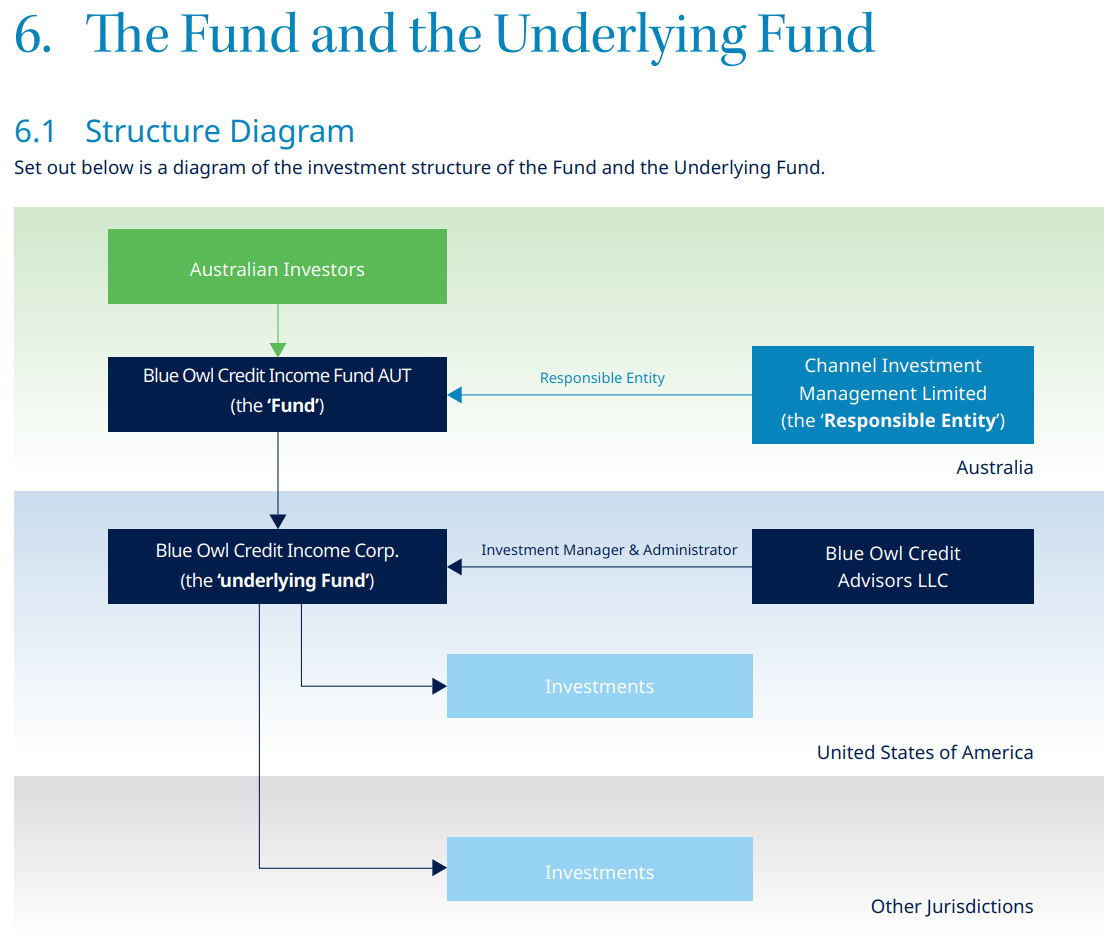

I’m not certain how many layers exist in this particular fund of funds, the infographic provided by the manager simply mentions “Investments” in both the USA and “Other Jurisdictions”, which is important, as the more layers, the more complex, the more layers of fees… That said, it’s quite standard for ‘Alternative assets’ to exist in these multi-layered structures for both Australia and abroad.

I have no idea and no comment on whether the ‘hurdles’ are high or not, I'm not an expert on the sector or the product.

As far as I can work out, the confusingly similar APIR Code CHN6006AU, the newer Alternative Credit Fund AUT, has a different fee structure.

Discount to NAV

It pays to note, performance fees on capital gains are further complicated when the asset’s valuation is subjective, like property, or private equity, or…. private credit… which is.. private and not traded like a listed share.

The “underlying fund” of the Australian investment is the Blue Owl Credit Income Corp. (‘OCIC’), is a closed end management investment company known as a business development company (‘BDC’).

As of April 3rd, according to Reuters, investors in the underlying Blue Owl BDC asked to pull 21.9% of shares in the three months ended March 31, according to an investor letter, up from 5.2% in the prior period. Those percentages rank among the highest quarterly redemption requests the industry has ever seen (noting another Blue Owl tech fund got 40.7% for the same quarter). This is happening across the industry but accoirding to Ratings House Moody’s, redemption request at Blue Owl are “significantly higher than peers”.

There is much discussion on the value of private credit investments, take for example OBDC II — Blue Owl Capital Corporation II, Hedge fund Saba Capital Management and secondary investor Cox Capital Partners commenced a tender offer to purchase up to $30.4 million in shares at $3.80 per share, representing a 34.9% discount to NAV after accounting for an upcoming dividend.

Blue Owl has both Listed and unlisted BDCs. One listed BDC is OBDC Listed Blue Owl BDC (NYSE: OBDC).

OBDC (as as time of writing, 14th April 2026) has a quoted share price of $10.75. (CNN).

Blue Owl’s Q4 2025 earnings filed Feburary 18th 2026 provide a “net Asset Value” aka ‘NAV’ of $14.81.

Thus, the reports of a discount north of 20% imply, that Investors don’t agree about the value of the Blue Owl’s ‘OBDC’. Management fees and performance fees are charged on the NAV - not traded values.

Are we all plucked?

On one hand, since the GFC (it has always existed but we exist in peak bubble-bear times) there has been an insatiable appetite amongst both morons and pundits to call the next bubble; this has kind of led to a ‘boy cries wolf’ type behavior.

Private Credit is relatively new, and thus, spooky, but, the levels of debt aren’t as bad as some think, but again, there’s a lot of it and it’s private, so we don’t know for certain.

On the other hand, a lot of smart people think there are serious and inherent issues, that have been bubbling away for a while, these issues could be compounded by economic headwinds thanks to one particular Orange Fuckhead and these will be compounded further by AI reshaping business, business with high levels of gearing to private credit funds.

If you haven’t heard this 999,999 times a day, well done, you’re living better than me.

Source: ADHD (Andy Darroch Home Downtime)

That being said, Howard Marks, probably the smartest person ever in credit gave what I thought was quite a balanced overview.

An excellent read (or listen, but the AI voice on the podcast was mildly disappointing; https://www.oaktreecapital.com/insights/memo/whats-going-on-in-private-credit)

Some funds will do worse than others. Some funds will do better than others.

Some investors might have to wait a while until they can get their money back.

Some might take a haircut.

Who knows, time will tell.

Personally, I would much, much, rather have my Blue Owl exposure via a big industry fund like NGS, who have a modest exposure to the whole firm, rather than the unbelievably convoluted fee and complicated fund of funds via a combination of Blue Owl, Channel Capital and Koda Capital.

Plenty Worse Birds & Plenty Worse Private Credit

An actual hectic blue bird.

Still, I have no doubt whatsoever that there’s far, far far worse Private Credit investments than Blue Owl, right on our shores.